California Water Files Definitive Proxy Materials and Sends Letter to SJW Group Stockholders

Reiterates Commitment to All-Cash $68.25 Per Share Proposal for SJW

Urges SJW Stockholders to Vote AGAINST the Connecticut Water Transaction Using the WHITE Proxy Card

SAN JOSE, Calif.--(BUSINESS WIRE)-- California Water Service Group (“California Water”) (NYSE:CWT) today announced that it has filed definitive proxy materials with the U.S. Securities and Exchange Commission and sent a letter to SJW Group (“SJW”) (NYSE: SJW) stockholders, along with a WHITE proxy card, in connection with SJW’s Special Meeting of Stockholders. California Water urges SJW stockholders to vote AGAINST the proposed merger of SJW and Connecticut Water (NYSE: CTWS) using the WHITE proxy card.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20180531006524/en/

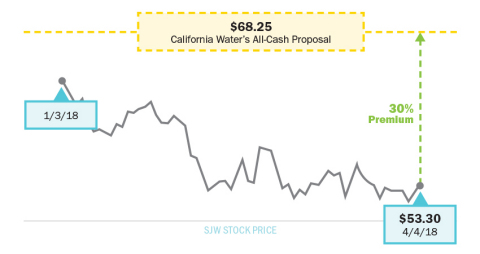

California Water's $68.25 Per Share Proposal Represents 30% Premium to SJW's Closing Stock Price On Date of Offer (Graphic: Business Wire)

On April 4, 2018, California Water made a proposal to acquire SJW for $68.25 per share in cash, which exceeds SJW’s all-time high closing share price, and represents a 30% premium to SJW’s share price at the time of California Water’s proposal.

Martin A. Kropelnicki, President and CEO of California Water, said: “We firmly believe our all-cash proposal, which was summarily rejected by the SJW Board, delivers superior and immediate value compared to the transaction with Connecticut Water in which SJW is paying a premium to Connecticut Water shareholders.1 SJW stockholders deserve the opportunity to voice their opinion on the future of SJW instead of being forced to accept an all-stock merger that we believe carries significant operational risk and is premised on vague and unspecified synergies. By voting on the WHITE proxy card AGAINST the SJW and Connecticut Water transaction, SJW stockholders can send a clear message to the San Jose Water Board that they should immediately engage in discussions with us regarding our compelling proposal.”

The full text of the letter to SJW stockholders follows:

ATTENTION SAN JOSE WATER GROUP (SJW) STOCKHOLDERS:

VOTE AGAINST SJW’S PROPOSED MERGER WITH CONNECTICUT WATER AND PROTECT YOUR OPPORTUNITY TO RECEIVE $68.25 PER SHARE IN CASH

TAKE ACTION TODAY!

May 31, 2018

Dear SJW Group Stockholder,

On April 4, 2018, we at California Water made a private proposal to acquire SJW for $68.25 per share in cash. This proposal marked the latest in a series of attempts to work constructively and privately with SJW’s Board regarding a potential business combination. Like each of our prior proposals, it was rejected outright by the SJW Board and management, who refused to even engage with us.

Instead of engaging with California Water, SJW Group’s Board has embarked on an ill-advised effort to merge with Connecticut Water, a water utility located over 3,000 miles away from SJW’s California footprint. Coincidentally, Eric Thornburg, SJW’s CEO, was the CEO of Connecticut Water for eleven years until he stepped down seven months ago, and because he has a substantially larger economic interest in Connecticut Water stock than San Jose Water stock, he is poised to benefit if the Connecticut Water merger is completed. We believe SJW stockholders should question if the SJW CEO’s personal financial interests are more aligned with enriching Connecticut Water shareholders than acting in the best interest of SJW stockholders.

We firmly believe that the proposed Connecticut Water transaction carries substantial operational risks, as SJW Group has itself acknowledged in public filings. And unlike the California Water proposal, the Connecticut Water transaction will provide no cash consideration to SJW stockholders: you will simply retain your current SJW share holdings, while paying Connecticut Water shareholders, including Mr. Thornburg, an 18% premium.2

We do not believe in the merits of a SJW/Connecticut Water transaction. Our $68.25 all-cash proposal is specifically conditioned on the termination of the SJW/Connecticut Water merger agreement.

In the coming weeks, SJW will be holding a special meeting of SJW stockholders to vote on the Connecticut Water merger. At this special meeting, you will have an important opportunity to send a clear message to the SJW Board that they should immediately engage in discussions with California Water to maximize the value of your investment.

For the reasons set forth below and in the enclosed materials, we urge you to vote AGAINST using the WHITE proxy card in order to reject the proposed all-stock merger with Connecticut Water.

WE BELIEVE CALIFORNIA WATER IS OFFERING YOU SIGNIFICANT AND IMMEDIATE VALUE THAT CONNECTICUT WATER CANNOT PROMISE

Our $68.25 per share ALL-CASH proposal:

- Exceeds SJW’s all-time high closing share price;

- Represents a 30% premium to SJW’s share price at the time of California Water’s April 4, 2018 proposal; and

- Provides stockholders with cash value immediately upon closing.

In contrast, in the proposed all-stock merger with Connecticut Water, you are paying a premium to Connecticut Water shareholders at closing.3 Additionally, it asks you to:

- Bear the substantial execution risk of operating two separate businesses located 3,000 miles apart in different regulatory environments, with zero quantification of anticipated synergies, if any.

- Hold out for promises of accretion that may never materialize, without offering – in our view – any concrete plans on how it will achieve this alleged “value.”

- Trust a CEO that, in our view, is conflicted as to this transaction, and still has limited insight into the California regulatory environment and rule setting as prescribed by the California Public Utilities Commission (CPUC).

WE BELIEVE CALIFORNIA WATER’S PROPOSAL OFFERS A CLEAR PATH TO CLOSING

Our proposal is not subject to any financing contingencies, and we are confident that we can conduct confirmatory due diligence and reach a definitive agreement within two weeks if we have the cooperation of the SJW Board and management.

In a desperate attempt to distract from the significant flaws in their merger with Connecticut Water, SJW has made various claims about our regulatory review process, which requires approvals in California and Texas. The fact is, we have worked collaboratively with the CPUC for many decades, and believe the unique customer, employee and community benefits that a California Water-SJW combination provides are self-evident – particularly given our strong operational track record in California.

Ultimately, we believe we can obtain all required regulatory approvals within eight months after submitting the requisite applications.

IN OUR VIEW THERE IS SIGNIFICANT UNCERTAINTY AND RISK IN CLOSING THE PROPOSED CONNECTICUT WATER MERGER

The SJW/Connecticut Water transaction faces regulatory approval in two different states – Connecticut and Maine. We believe that regulators in these states have no formal relationships with SJW given SJW’s lack of operations in either state and may have concerns over Connecticut Water’s ownership being transferred to an out-of-state company, which could delay the receipt of requisite approvals in one or both jurisdictions well beyond calendar year 2018.

Additionally, the mayor of San Jose believes the CPUC should review the merger with Connecticut Water and has communicated his views directly with the CPUC. These appeals to the CPUC are clearly being heard – CPUC Administrative Law Judge Karl Bemesderfer disclosed at a Public Participation Hearing on May 30, 2018 that CPUC’s legal division has decided to review the SJW/Connecticut Water transaction.

Finally, a third party, Eversource Energy, has submitted a proposal to acquire Connecticut Water and is soliciting proxies from Connecticut Water shareholders to vote against the SJW/Connecticut Water merger. As a result of the pressure from Eversource, Connecticut Water announced on May 31, 2018 an amendment to its merger agreement with SJW that allows it to conduct a 45-day go shop process, during which Connecticut Water can actively solicit alternative acquisition proposals from third parties. Since the SJW/Connecticut Water merger requires the approval of holders of two-thirds of the outstanding Connecticut Water common shares, we believe that the Eversource Energy proposal and solicitation, combined with the go shop period, create a high degree of uncertainty around the completion of the SJW/Connecticut Water merger.

SJW STOCKHOLDERS

VOTE THE WHITE PROXY CARD TODAY TO STOP SJW MANAGEMENT FROM FORCING THROUGH A SWEETHEART DEAL AT YOUR EXPENSE

By voting AGAINST using the enclosed WHITE proxy card, you can prevent a transaction we believe carries significant risks and gives only vague and unsupported promises of speculative value to SJW stockholders.

Vote AGAINST the SJW/Connecticut Water proposal. A rejection of the Connecticut Water merger proposal at the special meeting will send a clear message to the SJW Board that they should engage immediately in constructive discussions with California Water regarding our all-cash proposal.

Sincerely,

Martin A. Kropelnicki

President and Chief Executive Officer

|

If you have any questions or need assistance in voting your shares, please contact the firm assisting Cal Water in this solicitation: |

| INNISFREE M&A INCORPORATED |

| Stockholders May Call Toll Free: (888) 750-5834 |

| Banks and Brokers May Call Collect: (212) 750-5833 |

California Water’s proxy statement, stockholder letter and other materials related to SJW’s special meeting will be available at www.sjwvalue.com.

About California Water Service Group

California Water Service Group is the parent company of California Water Service, Washington Water Service, New Mexico Water Service, Hawaii Water Service, CWS Utility Services, and HWS Utility Services. Together, these companies provide regulated and non-regulated water service to approximately 2 million people in more than 100 California, Washington, New Mexico, and Hawaii communities. California Water Service Group’s common stock trades on the New York Stock Exchange under the symbol “CWT.” Additional information is available online at www.calwatergroup.com.

Forward-Looking Statements

This news release contains forward-looking statements within the meaning established by the Private Securities Litigation Reform Act of 1995 (“Act”). The forward-looking statements are intended to qualify under provisions of the federal securities laws for “safe harbor” treatment established by the Act. Forward-looking statements are based on currently available information, expectations, estimates, assumptions and projections, and management’s judgment about the Company, the water utility industry and general economic conditions. Such words as would, expects, intends, plans, believes, estimates, assumes, anticipates, projects, predicts, forecasts or variations of such words or similar expressions are intended to identify forward-looking statements. The forward-looking statements are not guarantees of future performance. They are subject to uncertainty and changes in circumstances. Actual results may vary materially from what is contained in a forward-looking statement. Factors that may cause a result different than expected or anticipated include, but are not limited to: the failure to consummate the proposed transaction with SJW upon the terms set forth in California Water’s proposal; governmental and regulatory commissions’ decisions; changes in regulatory commissions’ policies and procedures; the timeliness of regulatory commissions’ actions concerning rate relief; changes in environmental compliance and water quality requirements; electric power interruptions; changes in customer water use patterns and the effects of conservation; the impact of weather and climate on water availability, water sales and operating results; civil disturbances or terrorist threats or acts, or apprehension about the possible future occurrences of acts of this type; labor relations matters as we negotiate with the unions; restrictive covenants in or changes to the credit ratings on our current or future debt that could increase our financing costs or affect our ability to borrow, make payments on debt or pay dividends; and, other risks and unforeseen events. When considering forward-looking statements, you should keep in mind the cautionary statements included in this paragraph, as well as our annual 10-K, Quarterly 10-Q, and other reports filed from time-to-time with the Securities and Exchange Commission. California Water assumes no obligation to provide public updates of forward-looking statements except to the extent required by law.

Important Additional Information

Today California Water filed a definitive proxy statement with the Securities and Exchange Commission (the “Definitive Proxy Statement”) to solicit proxies in opposition to resolutions related to the pending merger between SJW Group and Connecticut Water Service, Inc. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT AND ANY OTHER DOCUMENTS TO BE FILED WITH THE SECURITIES AND EXCHANGE COMMISSION, WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. All such documents, if filed, would be available free of charge at the Securities and Exchange Commission’s website (www.sec.gov) or by directing a request to Innisfree M&A Incorporated at (888) 750-5834 (banks and brokers call collect at (212) 750-5833).

Participants in the Solicitation

California Water, its directors and certain of its officers and employees may be deemed to be participants in any solicitation of SJW Group stockholders in connection with the proposed transaction between California Water and SJW Group. Information about such participants, and a description of their direct or indirect interests, by security holdings or otherwise, is included in the Definitive Proxy Statement.

|

_________________________ |

| 1 We note that the matter subject to approval by SJW’s stockholders is the issuance of additional shares to Connecticut Water (not the receipt of additional consideration). |

|

2 Based on the relative closing price of SJW and Connecticut Water shares on the last trading day prior to the announcement of the proposed Connecticut Water merger. |

| 3 We note that the matter subject to approval by SJW’s stockholders is the issuance of additional shares to Connecticut Water (not the receipt of additional consideration). |

Released May 31, 2018