California Water Sends Letter to SJW Stockholders Outlining Significant Governance Concerns at SJW

Urges SJW Stockholders to Vote AGAINST Connecticut Water Transaction Using WHITE Proxy Card

SAN JOSE, Calif.--(BUSINESS WIRE)-- California Water Service Group (“California Water”) (NYSE:CWT) today sent a letter to SJW Group (“SJW”) (NYSE:SJW) stockholders, along with a WHITE proxy card, in connection with SJW’s upcoming Special Meeting of Stockholders. The letter outlines serious corporate governance concerns about SJW, which provide further reasons for SJW stockholders to vote AGAINST the proposed all-stock merger between SJW and Connecticut Water (NYSE:CTWS) using the WHITE proxy card.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20180625005598/en/

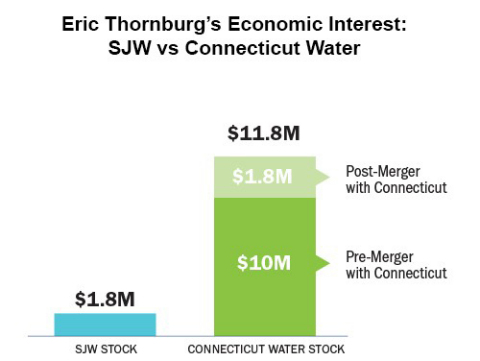

Reflects SJW and Connecticut Water share prices as of June 22, 2018; reflects ownership stake, assuming consummation of the merger, the agreed-upon exchange ratio of 1.1375 and SJW's share price as of June 22, 2018

On April 4, 2018, California Water made a proposal to acquire SJW for $68.25 per share in cash, which exceeds SJW’s all-time high closing share price, and represents a 30% premium to SJW’s share price at the time of California Water’s proposal.

California Water’s proxy statement, stockholder letter and other materials related to SJW’s special meeting are available at www.sjwvalue.com.

The full text of the letter that was sent to SJW stockholders follows:

June 25, 2018

Dear SJW Group Stockholder,

We at California Water have made a good faith offer to acquire SJW Group for $68.25 per share in cash, which delivers substantial value to you. We strongly believe that our proposal is superior to the so-called “merger of equals” with Connecticut Water, which SJW’s management vehemently endorses.

Specifically, we believe our proposal:

- Offers SJW stockholders a significant premium and value that exceeds SJW’s all-time high closing price;

- Provides value that is not contingent on vague promises of future accretion; and

- Has a clear path to completion, requiring regulatory review in only two states, aside from customary closing conditions.

However, the SJW Board has persistently refused to discuss a potential transaction with California Water, let alone engage with us in a meaningful way. Instead, since delivery of our private proposal in April 2018, SJW has engaged in a hostile public attack against California Water’s reputation and its stakeholders.

It is curious and troubling that our superior, all-cash proposal would cause such a visceral reaction on the part of SJW’s Board and management.

ARE SJW’S ACTIONS GUIDED BY THE PERSONAL AND FINANCIAL MOTIVATIONS OF A CONFLICTED BOARD & MANAGEMENT TEAM?

We believe it is important that SJW stockholders consider the following facts, as they might explain why SJW is so adamant about consummating a transaction with Connecticut Water and refusing to engage with California Water:

- SJW’s current CEO, Eric Thornburg, was the CEO of Connecticut Water for over 11 years: He only stepped down in November 2017, four months before SJW announced its merger with Connecticut Water, to become CEO of SJW. The “merger of equals” appears to be nothing more than the SJW CEO bringing together his current and former companies at the expense of SJW stockholders. The transaction was negotiated under conflicted circumstances that, in our view, the Board should not have allowed.

-

SJW’s CEO has a significantly higher financial stake in Connecticut Water stock than he does in SJW stock and is therefore conflicted: The value of the Connecticut Water stock that he currently owns is approximately five times more than the value of his SJW stock. Financially, he stands to benefit much more as a Connecticut Water shareholder than as an SJW stockholder. This creates what is, in our view, a massive conflict of interest.

This is shocking enough, but when you combine it with the fact that SJW stockholders are receiving NO premium in this transaction1 – rather, they are paying a premium to Mr. Thornburg and other Connecticut Water shareholders – it raises serious questions about whose interests he is looking out for—SJW stockholders, or Connecticut Water shareholders.

-

Mr. Thornburg spent more time negotiating the deal on behalf of Connecticut Water than SJW: The negotiations between SJW and Connecticut Water began in June 2016, when Mr. Thornburg was President and CEO of Connecticut Water. In November 2017, Mr. Thornburg took the helm as CEO of SJW and immediately resumed his duties as negotiator, only this time representing SJW, until the transaction was announced four months later.

Under those circumstances, we seriously question the effectiveness of Mr. Thornburg as a negotiator on behalf of SJW stockholders.

-

We believe Mr. Thornburg should have abstained from participating in negotiations with Connecticut Water: Neither Mr. Thornburg’s recent long tenure at Connecticut Water, nor his significantly higher financial stake in Connecticut Water, appears to have given any member of the SJW Board or Mr. Thornburg second thoughts about allowing him to lead in negotiations with his former colleagues at Connecticut Water, or in Board discussions regarding the “merger of equals.” We believe it is no surprise that, as a director of SJW, he supported a merger with his former employer, including the millions of dollars in “change of control” provisions that benefit his former colleagues at Connecticut Water if they lose their jobs.

In short, it appears that Mr. Thornburg negotiated a transaction with his “Connecticut Water hat” on and then agreed to it as CEO of SJW.

-

The exchange ratio for the SJW-Connecticut Water transaction is based on a lower cost of capital decision – further benefiting Connecticut Water and Mr. Thornburg: In February 2018, the CPUC, SJW’s California utility regulator, issued a proposed decision to reduce SJW’s authorized cost of capital, which would reduce SJW’s authorized revenue by approximately $10 million for 2018. Following this development, SJW agreed to amend the exchange ratio and improve it for the benefit of Connecticut Water shareholders.

On March 22, 2018, following the announcement of the Connecticut Water merger, the CPUC issued a final decision providing a less severe reduction to SJW’s authorized cost of capital. There is no indication whatsoever that SJW’s financial forecasts were subsequently updated to reflect this more positive outcome, nor was the exchange ratio updated to reflect this development.

Why wouldn’t the SJW Board renegotiate the terms of the Connecticut Water deal after the CPUC issued its final decision benefiting SJW? Why would they only renegotiate when it behooves Connecticut Water shareholders? And, more shockingly, why would the SJW Board not disclose to its stockholders the forecasts from the final cost-of-capital decision?

-

We believe SJW’s Lead “Independent” Director is conflicted and has unique incentives to do a stock deal with Connecticut Water: SJW’s Lead Independent Director, Robert A. Van Valer, has recently touted his status as SJW’s largest stockholder when announcing his support for the Connecticut Water transaction. In critiquing a potential transaction with California Water, he has highlighted the fact that an all-cash transaction would not be tax-free. In that regard, we believe that his position as a 30-plus year stockholder with a very low cost-basis in SJW stock creates a severe misalignment of incentives between him and a majority of other stockholders, whom we believe on average have a significantly higher cost basis.

As a board member, Mr. Van Valer has a fiduciary duty to all stockholders, not just the family trust vehicles that he serves.

WE BELIEVE THE SJW BOARD HAS BEEN LESS THAN UPFRONT WITH ITS STOCKHOLDERS

In our view, the SJW Board and management team owe some answers to their stockholders. For example:

- Why is the SJW Board critical of the all-cash nature of California Water’s proposal, when it previously summarily rejected a stock proposal from California Water? SJW has criticized our proposal for being all-cash, claiming you will lose out because a cash offer is taxable and that their stock deal at a lower value is somehow worth more than cash. However, SJW conveniently disregards the fact that when we previously attempted to engage with the SJW Board in September 2017, we offered the option of cash, stock, or a combination thereof in a transaction at a 25-30% premium to SJW’s then-current stock price – and SJW still refused to engage.

- Why did it take SJW one full week to publicly disclose that it had received a letter from the California regulators – the CPUC – demanding that SJW seek regulatory approval in California to complete the Connecticut Water transaction? SJW has previously used CPUC review as a reason not to consider a potential combination with California Water, complaining that CPUC review could take up to 18 months. Now that its “merger of equals” requires the same and additional regulatory reviews, we will be curious to see if SJW changes its tune with regard to reasons against our proposal.

- Why has SJW not disclosed the financial analyses performed by its financial advisor in connection with rejecting our offer? We continue to look for any detail about the financial analyses and metrics used by SJW’s financial advisor to recommend the rejection of our offer. Was any effort made to quantify the value of our offer against the Connecticut Water transaction, or is the lack of a public disclosure of their financial analysis an indication that the Connecticut Water deal does not make economic sense when objectively compared to our offer?

- Was SJW’s financial advisor unable to deliver an inadequacy opinion regarding our offer? SJW stockholders should question the reasons why there is no mention by the SJW Board of a request for an inadequacy opinion from its financial advisor as it relates to our offer. We believe that our offer is so compelling to SJW stockholders that SJW’s bankers were simply unable to conclude our offer was inadequate.

PROTECT YOUR INVESTMENT

VOTE “AGAINST” USING THE WHITE PROXY CARD TODAY

TO STOP SJW’S BOARD

FROM PUSHING THROUGH A SELF-INTERESTED DEAL

We stand ready to engage with the SJW Board regarding a transaction between our two companies that will deliver substantial value to SJW stockholders.

In today’s world, investor-owned utilities should be held to the highest standards of transparency, sustainability, service and good corporate governance. Given this and the substantial value and premium we have offered to SJW, as well as our record of flexibility regarding the components of a transaction, it is disappointing that the SJW Board has, in our view, continued to pursue a path of entrenchment to the detriment of its stockholders.

Sincerely,

Martin A. Kropelnicki

President and Chief Executive Officer

|

If you have any questions or need assistance in voting or tendering your shares, please contact the firm assisting California Water: |

| INNISFREE M&A INCORPORATED |

| Stockholders May Call Toll Free: (888) 750-5834 |

| Banks and Brokers May Call Collect: (212) 750-5833 |

About California Water Service Group

California Water Service Group is the parent company of California Water Service, Washington Water Service, New Mexico Water Service, Hawaii Water Service, CWS Utility Services, and HWS Utility Services. Together, these companies provide regulated and non-regulated water service to approximately 2 million people in more than 100 California, Washington, New Mexico, and Hawaii communities. California Water Service Group’s common stock trades on the New York Stock Exchange under the symbol “CWT.” Additional information is available online at www.calwatergroup.com.

Forward-Looking Statements

This news release contains forward-looking statements. Forward-looking statements are based on currently available information, expectations, estimates, assumptions and projections, and management’s judgment about the Company, the water utility industry and general economic conditions. Such words as would, expects, intends, plans, believes, estimates, assumes, anticipates, projects, predicts, forecasts or variations of such words or similar expressions are intended to identify forward-looking statements. The forward-looking statements are not guarantees of future performance. They are subject to uncertainty and changes in circumstances. Actual results may vary materially from what is contained in a forward-looking statement. Factors that may cause a result different than expected or anticipated include, but are not limited to: the failure to consummate the proposed transaction with SJW upon the terms set forth in California Water’s proposal; governmental and regulatory commissions’ decisions; changes in regulatory commissions’ policies and procedures; the timeliness of regulatory commissions’ actions concerning rate relief; changes in environmental compliance and water quality requirements; electric power interruptions; changes in customer water use patterns and the effects of conservation; the impact of weather and climate on water availability, water sales and operating results; civil disturbances or terrorist threats or acts, or apprehension about the possible future occurrences of acts of this type; labor relations matters as we negotiate with the unions; restrictive covenants in or changes to the credit ratings on our current or future debt that could increase our financing costs or affect our ability to borrow, make payments on debt or pay dividends; and, other risks and unforeseen events. When considering forward-looking statements, you should keep in mind the cautionary statements included in this paragraph, as well as our annual 10-K, Quarterly 10-Q, and other reports filed from time-to-time with the Securities and Exchange Commission. California Water assumes no obligation to provide public updates of forward-looking statements except to the extent required by law.

1 Consider in this regard that the matter subject to approval by SJW's stockholders is the issuance of additional shares to Connecticut Water shareholders (not the receipt of additional consideration)

Released June 25, 2018